Credit scores are an essential aspect of personal finance. They are the numerical representation of an individual’s creditworthiness, and they play a crucial role in determining the likelihood of obtaining credit. Understanding how credit scores are calculated can help individuals make informed financial decisions and improve their credit scores. In this article, we will discuss the factors that go into calculating credit scores and provide tips for maintaining a healthy credit score.

Table of Contents

- Introduction

- What is a credit score?

- Why is a credit score important?

- How are credit scores calculated?

- Payment history

- Credit utilization

- Length of credit history

- Types of credit

- New credit

- How to check your credit score

- Tips for improving your credit score

- Pay bills on time

- Keep credit utilization low

- Maintain a mix of credit

- Limit new credit applications

- Conclusion

- FAQs

1. Introduction

A credit score is a numerical value that ranges from 300 to 850, which represents an individual’s creditworthiness. This score is determined based on various factors such as payment history, credit utilization, length of credit history, types of credit, and new credit. In this article, we will discuss in detail how credit scores are calculated and provide tips for maintaining a healthy credit score.

2. What is a credit score?

A credit score is a three-digit number that represents an individual’s creditworthiness. This score is calculated by credit bureaus, such as Equifax, Experian, and TransUnion, based on information provided by lenders, banks, and other financial institutions. The credit score is determined by analyzing an individual’s credit report, which includes information such as payment history, credit utilization, length of credit history, types of credit, and new credit.

3. Why is a credit score important?

Credit scores are essential because they play a crucial role in determining an individual’s ability to obtain credit, such as loans, credit cards, and mortgages. A high credit score indicates that an individual is less of a risk to lenders and financial institutions, making it easier for them to obtain credit with favorable terms and interest rates. On the other hand, a low credit score indicates that an individual is a higher risk to lenders, making it difficult for them to obtain credit, and often with less favorable terms and higher interest rates.

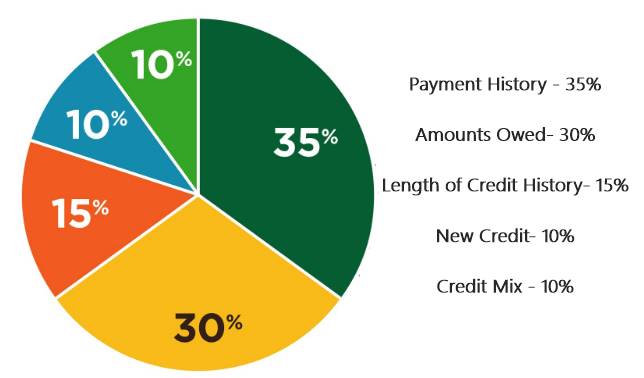

4. How are credit scores calculated?

Credit scores are calculated based on various factors, including payment history, credit utilization, length of credit history, types of credit, and new credit.

Payment history

Payment history is one of the most critical factors in determining an individual’s credit score, accounting for 35% of the total score. Lenders and financial institutions want to see that an individual has a history of paying bills on time. Late or missed payments can significantly impact an individual’s credit score and can remain on their credit report for up to seven years.

Credit utilization

Credit utilization is the amount of credit an individual is using compared to their credit limit. This factor accounts for 30% of the credit score. Lenders prefer to see individuals using less than 30% of their available credit, as high credit utilization indicates an increased risk of default.

Length of credit history

The length of credit history accounts for 15% of the credit score. The longer an individual has been using credit, the more reliable they are to lenders. This factor considers the age of the individual’s credit accounts, the length of time since their last account activity, and the average age of all their accounts.

Types of credit

The types of credit an individual has used accounts for 10% of the credit score. Lenders prefer to see a mix of credit types, such as credit cards, loans, and mortgages. This factor indicates an individual’s ability to manage various types of credit.

New credit

New credit accounts for 10% of the credit score. Lenders want to see that an individual is not taking on too much new credit at once, as this can indicate a financial struggle. Applying for multiple new credit accounts in a short period can negatively impact an individual’s credit score.

5. How to check your credit score

Individuals can check their credit score by obtaining a free credit report from one of the three major credit bureaus: Equifax, Experian, and TransUnion. The Fair Credit Reporting Act entitles individuals to one free credit report every 12 months from each of the three credit bureaus. It is important to review the credit report regularly to ensure accuracy and identify any errors or fraudulent activity.

6. Tips for improving your credit score

Maintaining a healthy credit score is essential for obtaining credit with favorable terms and interest rates. Here are some tips for improving credit scores:

Pay bills on time

Late or missed payments significantly impact credit scores. It is crucial to pay bills on time to maintain a healthy credit score.

Keep credit utilization low

High credit utilization indicates an increased risk of default. Individuals should aim to use less than 30% of their available credit to maintain a healthy credit score.

Maintain a mix of credit

Lenders prefer to see a mix of credit types, such as credit cards, loans, and mortgages. This factor indicates an individual’s ability to manage various types of credit.

Limit new credit applications

Applying for multiple new credit accounts in a short period can negatively impact credit scores. Individuals should limit new credit applications to maintain a healthy credit score.

7. Conclusion

Credit scores play a crucial role in determining an individual’s creditworthiness. They are calculated based on various factors, including payment history, credit utilization, length of credit history, types of credit, and new credit. Maintaining a healthy credit score is essential for obtaining credit with favorable terms and interest rates. Individuals can check their credit score regularly and follow tips such as paying bills on time, keeping credit utilization low, maintaining a mix of credit, and limiting new credit applications to maintain a healthy credit score.

8. FAQs

- What is a good credit score?

- How long does it take to improve a credit score?

- Can paying off debt improve my credit score?

- How often should I check my credit score?

- How long do negative items stay on a credit report?

Answers to FAQs

- A good credit score is typically 670 or above.

- Improving a credit score can take several months or even years, depending on the individual’s credit history.

- Paying off debt can positively impact credit scores, as it improves credit utilization and payment history.

- It is recommended to check credit scores regularly, at least once a year, to ensure accuracy and identify any errors or fraudulent activity.

- Negative items, such as late or missed payments, can remain on a credit report for up to seven years, while bankruptcy can remain on a credit report for up to ten years.